Navigating the August Storm

The global financial system faces a critical test in August 2025 as the U.S. Treasury's cash reserves approach zero, forcing potentially $940 billion in bond issuance into markets already fragile from political uncertainty. This confluence of events creates a three-phase investment roadmap that different investor types must navigate carefully.

The Near-Term Storm (July-October 2025)

Despite widespread fears about the end of U.S. exceptionalism following January's inauguration, capital flows have remained surprisingly robust. Foreign investors continue buying U.S. assets, with Q1 2025 recording the sixth-largest inflows on record. However, this stability masks underlying fragility.

The U.S. Treasury General Account, currently at $301 billion, will be exhausted by early August. With the government facing its largest seasonal deficits in August-September, massive issuance must hit markets precisely when they're most vulnerable. History suggests trouble: when yields breach 5%, "things start to break," as witnessed in late 2021 and September 2023.

European banks, engaged in stealth quantitative easing, and Asian exporters recycling trade surpluses have supported treasuries. But this support may crumble under the weight of supply. Rising real yields amid Chinese deflation could trigger a "deflation scare," testing foreign investors' commitment to U.S. assets.

The Medium-Term Response (Q4 2025-2026)

Policymakers won't tolerate economic disruption. Expect the Federal Reserve to implement yield curve control or "funding for growth" programs—essentially QE by another name. Europe is already there, with the ECB engineering money creation through commercial bank bond purchases. This coordinated monetary response will initially spark a "reflation trade," lifting all boats.

However, this sets the stage for a second inflation wave, potentially worse than the 1970s sequel. While the dollar won't lose reserve status—there's no alternative—the world will gradually abandon reserve accumulation in favour of flexible exchange rates and domestic stability.

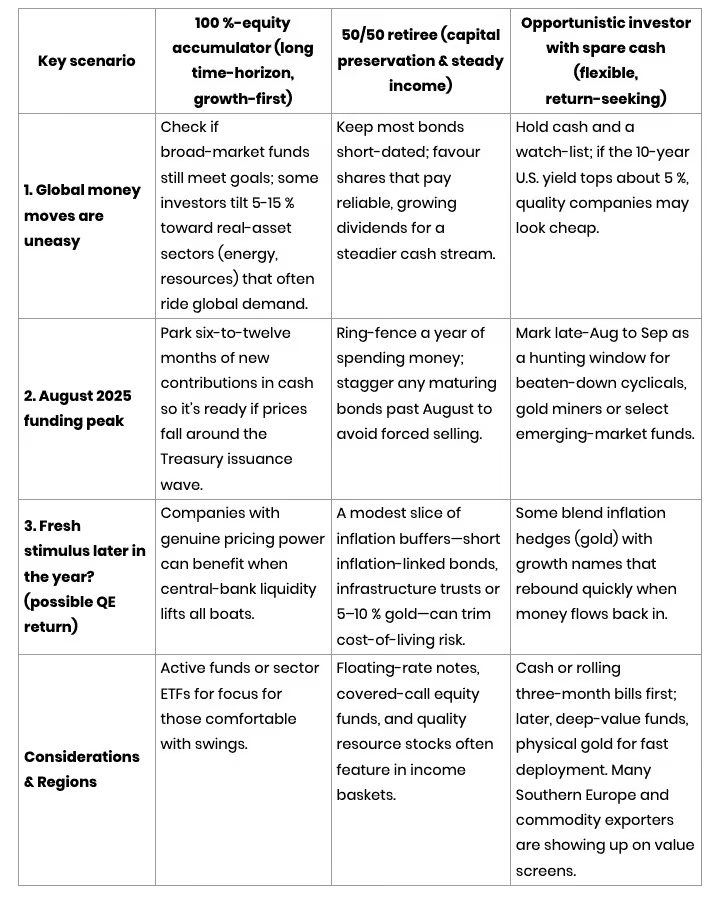

How To Use These Insights With Your Clients.

We have put together some talking points that advisers could use with clients. Usually we like to talk in terms of scenarios and probabilities but

1) we think there is a reasonable probability that the U.S. debt funding scenario that Hunt Economics has laid out will eventuate in some form

2) we accept that this approach can seem ‘mealy mouthed' at times, they want to know what you or we really think!

That said, there is every chance that the world will appear very different in a few short months, this timeline and the actions it implies will be superseded, especially given the uncertainty that policy making in the U.S. is currently creating. With all that in mind it is a fair question for clients to ask if we have a game plan given some of the headlines they may be reading about deficit spending in the U.S. As Mikel Tyson, the bard of boxing, once said “Everyone has a plan until they get punched in the head”!