Time to Reassess Their Place in Your Portfolio Strategy

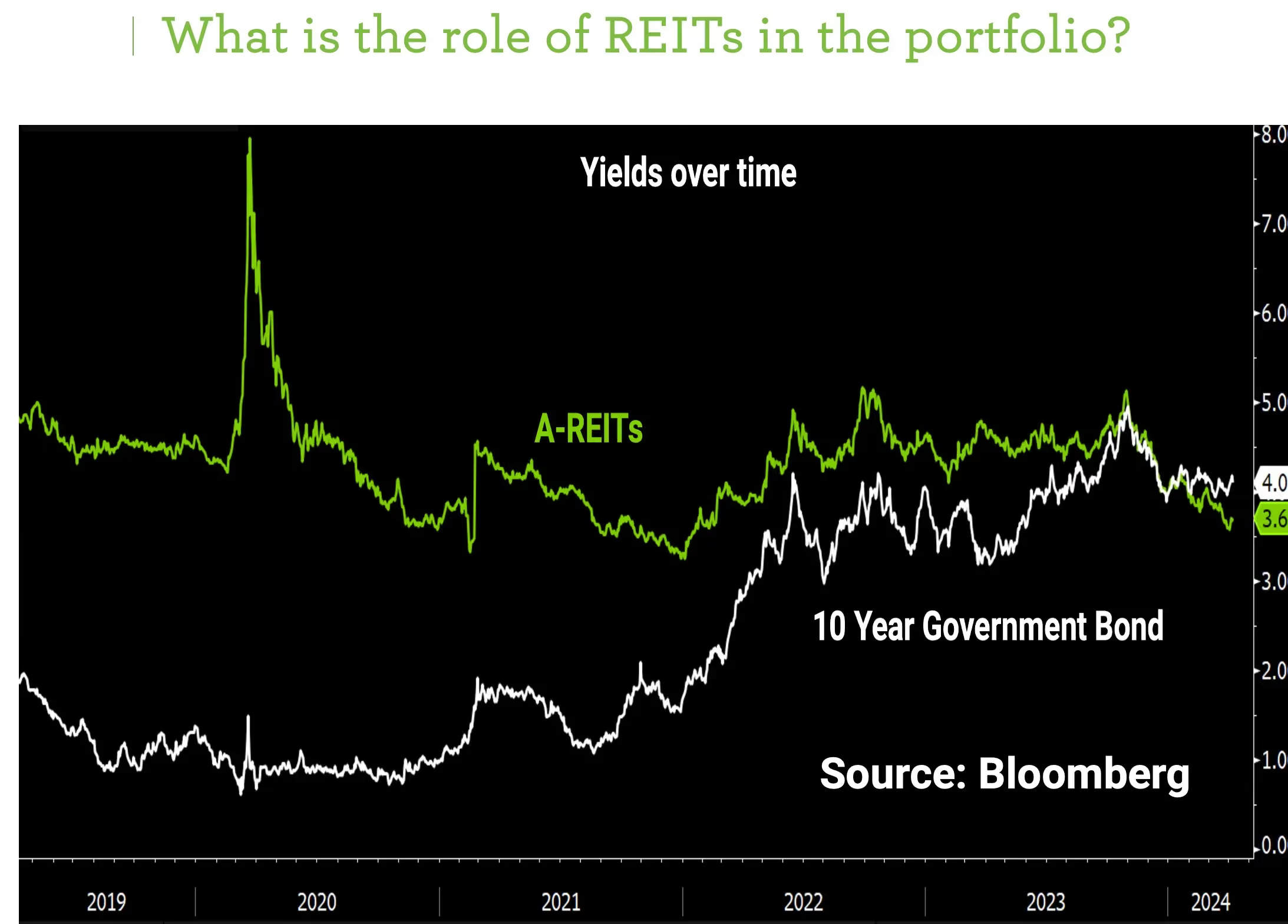

For many Australian investors, Real Estate Investment Trusts (A-REITs) have long been a staple of their portfolios, prized for their income generation potential. However, recent trends in the A-REIT space are prompting a reevaluation of the role these securities play and whether traditional approaches to A-REIT investing remain appropriate.

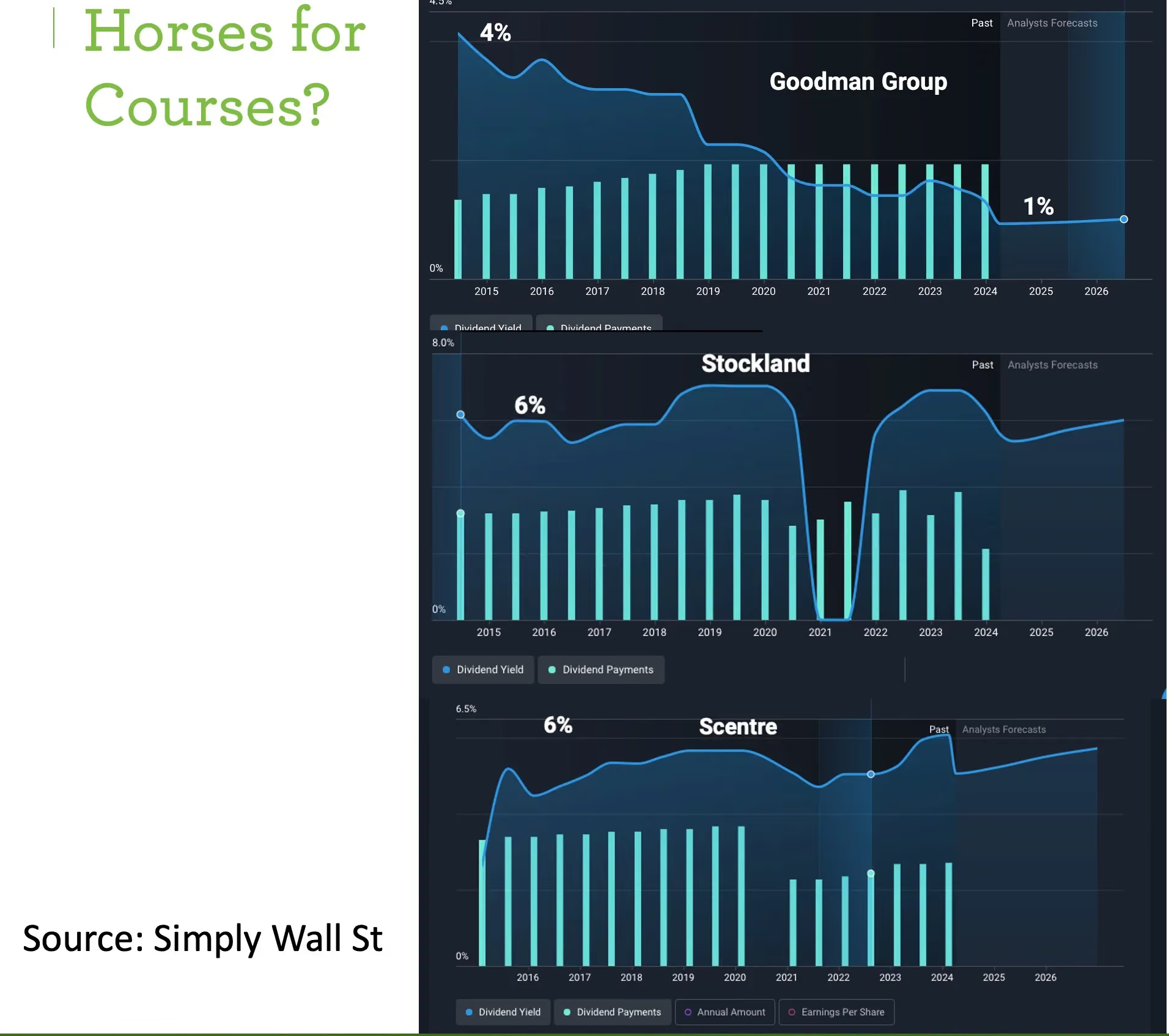

One key development is the growing dominance of Goodman Group within the A-REIT index. This low-yielding growth stock, focused on building out AI and data center infrastructure, now comprises nearly 40% of the index and trades at a lofty premium to book value. The outsized influence of Goodman has contributed to a highly polarized A-REIT market, with industrial REITs surging while retail and diversified REITs have posted more modest gains and office REITs have languished. To put this in context of the 14% rise in the A-REIT index this year 10.5% was attributable to Goodman, so if you were an active manager then this pretty much defined your relative performance. If you are passive investor the nature of the risk premium you are looking to capture has shifted considerably.

So, this divergence raises questions about the suitability of the A-REIT index as a passive investment vehicle and the effectiveness of active management in navigating such a bifurcated landscape. With Goodman's yield now at just 1% and little prospect for near-term dividend growth, investors may need to look elsewhere if income is their primary objective.

For those seeking a more balanced exposure to the sector or aiming to capitalize on the growth potential in segments like industrial properties, an actively managed approach or targeted sub-sector bets may be worth considering. Of course, the merits of active management must be weighed against the challenges of consistently outperforming in a market where a single stock can have such an outsized impact.

Ultimately, the decision of how to approach A-REIT investing will depend on each portfolio's context and objective but, most importantly, the intended role of A-REITs in the portfolio. In Australia we are used to dealing with index concentration, particularly in this space (Westfield was once 50% of the index) but now it has become clear that the days of treating A-REITs as a homogeneous, income-oriented asset class may be over. We will be circulating a paper on this topic in the coming weeks but in the meantime you can see some more charts and analysis on this topic in our Weekly Video.