What we are working on

On Bitcoin

As we have mentioned we are working on a few comms pieces in the wings, including our long-term outlook and Valuation Dashboard Update but nothing to show for it this week. Instead we are going discuss a subject that has started to crop up quite although it would be stretching things to say we had done much work on it, that is crypto currency and bitcoin in particular.

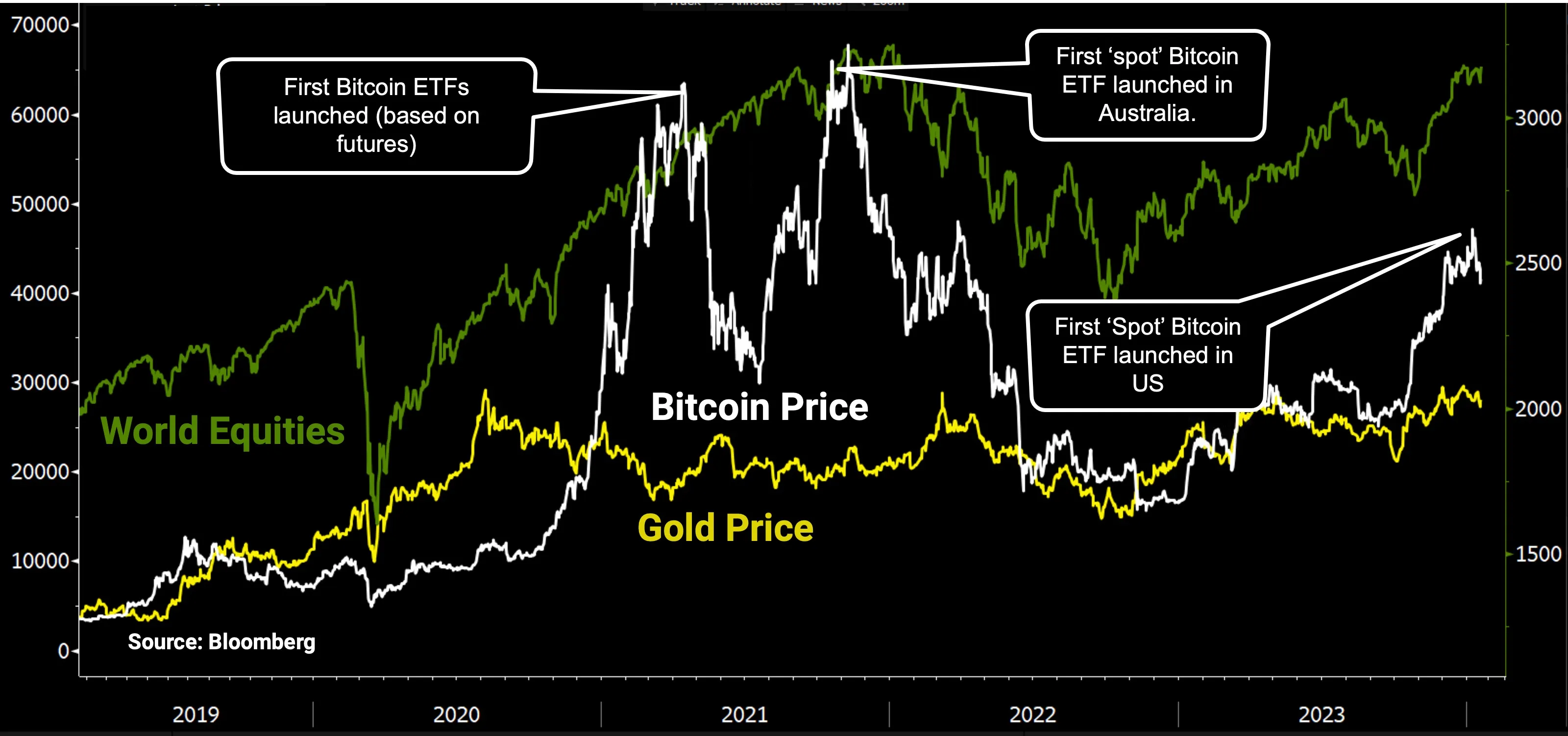

This is likely to come up because the Securities and Exchange Commission. (SEC) in the US just approved the first so-called ‘Spot' bitcoin ETFs and they have just started trading. The hope for many is that now the asset class will really take-off as it is much easier for investors to participate (much as the gold price spiked 20 years ago with the launch of the first gold ETF. Up until now Bitcoin ETF’s were constructed using bitcoin futures which led to deviations in performance (mainly to the downside). However, for Australian investors the announcement is a bit of a damp squib for investors in Australian and Europe as ‘spot’ Bitcoin ETF’s have been available for the last 18 months. Perhaps not completely coincidentally that time period also coincided with an almost 50% drawdown and the take-up so far has been fairly lacklustre. Ominously the US based variants are down 10% since launch 10 days ago.

The chart above suggests that euphoric crypto product launches do not necessarily portend outsized gains and it also points to the extreme volatility of the asset (and most crypto investments including so called ‘stable coins’). Which leads us to what advisers probably want to hear from us. From the questions we have received we think that breaks down to the following:

- Do we think Crypto is an investable asset class for SMA’s?

- If so how much would we put in an SMA and under what circumstances?

- If not, what should I say to an individual investor who wants to invest in Bitcoin?

Do we think Crypto is an investable asset class for SMA’s?

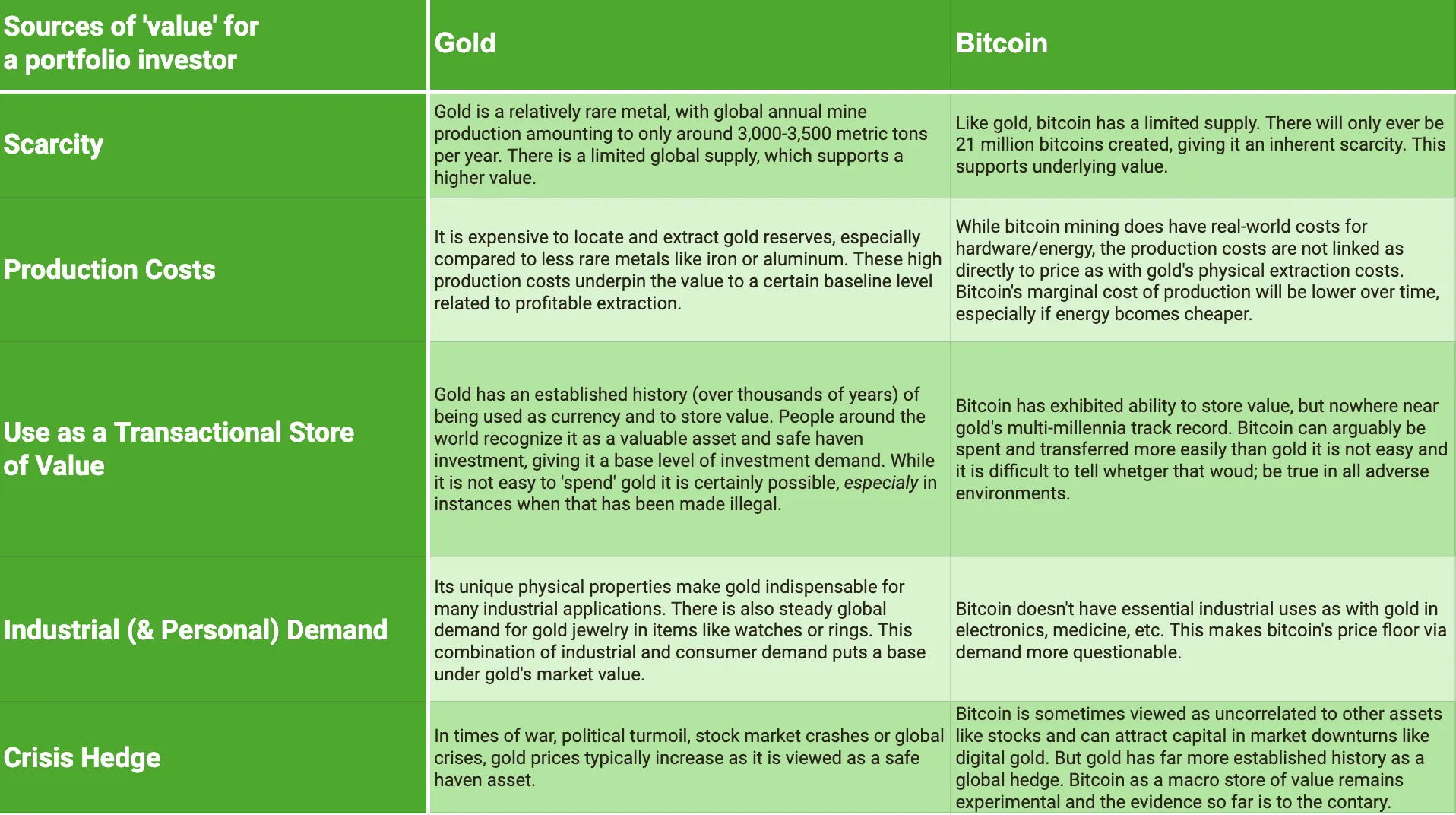

As important (and hopefully trusted) service providers to advisers that are themselves fiduciaries (using the term loosely) to retail clients we think we have a duty to have a ‘reasonable basis’ for making any investment decision, one that not only we can explain to our clients but that they can also explain to their clients. We call this ‘the chain of understanding’. In general this is based around three questions - what are the likely cash flows, how much are they likely to grow by and are they cheap or expensive on an historical or forward looking basis (based on reasonable assumptions). Already we run into problems with gold or even commodities as they don’t produce cash flows but the last part gives us an opening. They have a base value based on scarcity and industrial use as well as a fair amount of history. The following table ranks gold alongside Bitcoin on that basis:

On that basis we would still find it difficult to justify putting Bitcoin in an SMA portfolio at present. Arguably this is a tale tailored towards Gold as the incumbent in this space so we have tried to do some lateral thinking around what a more forward looking framework for thinking about cryptocurrency might look like. The best rationale we can come up with relates to the weaknesses of fiat (government sponsored) currencies and the potential that these might be undermined buy the deficit spending binge that the world (and especially) the US is experiencing. Perhaps the best and most institutionally credible proponent of that might be Michael Howell of Cross Border Capital. If you are interested in finding out more here is a good discussion with Michael on the Forward Guidance podcast but in short Howell sees cryptocurrencies, especially Bitcoin, emerging as a monetary hedge for younger generations in the context of ongoing monetary inflation. He draws a parallel to the Weimar Germany hyperinflation, where younger generations used equities to hedge while older generations held bonds and saw their wealth diminish.

While gold has traditionally been viewed as a hedge against monetary inflation, Howell suggests Bitcoin may now play that role for millennials and younger investors who find gold too "archaic". He sees cryptos as "fantastic monetary hedges."

So in an environment where Howell expects global liquidity to continue rising with possibly higher inflation over the medium-term, he believes Bitcoin and crypto have appeal as an alternative to traditional "safe assets" like government bonds. The rising popularity of crypto also seems tied to the expansionary policies of central banks like the Federal Reserve. In essence, Howell makes the bull case for Bitcoin and crypto as viable asset classes for hedging the inflationary impacts of rising liquidity and accommodative monetary policy. He sees further upside potential for cryptocurrencies. The only thing we would add to that is that the recent evidence is that equities also benefit from increasing liquidity which explains why Bitcoin is really not a great hedge and instead adds volatility with less predictability. Referring to the price chart above, when governments flooded the world with liquidity during COVID Bitcoin increased ten fold but when they started tightening policies it gave most of those gains back and when it started to seep back into the system, mainly via the US Overnight Reverse Repo Facility (see last week’s Weekly) it recovered again. For now that answers the second question for us for the foreseeable further (should we include its in SMA’s) as it looks much more like an accelerant of the current liquidity regime than a hedge against it. If it does look like we are reaching some kind of an end-game the current cycle and one wanted a hedge against the implosion of the current US sponsored global financial system this might be worth reevaluating but we are probably not there yet.

What should I say to an individual investor who wants to invest in Bitcoin?

Moving to the last question we obviously can’t be seen to be giving that sort of advice no matter how general this newsletter is and give the that it is written for advisers and not retail investors who may have all sorts of individual circumstances and personal views. Instead we thought it would be more fun to use AI to defer to fictional version economist (who might hold the same views as the one mentioned above) and Charlie Munger (RIP) who was perhaps, before his recent death, the most well known and passionate critic of crypto currency.

“The audience muttered anxiously as Charlie Munger and Michael Howell took the stage, the two titans known for their strong and opposing views on cryptocurrency. After quick introductions, the moderator jumped right in:

"Mr. Munger, you've been an outspoken critic of cryptocurrencies like Bitcoin, once calling them 'crypto crap.' Can you summarize why you think cryptos should be banned?"

Munger scowled. "Crypto is worthless gambling with insane speculation. It's a con game that has no underlying value or use to civilization. Speculators are lured in by promises of getting rich quick, while the crypto insiders rig the game to benefit themselves through pre-mining and shady exchanges. The fact that government allows this casino to operate is crazy and shameful!"

The moderator turned to the widely respected economist. "A rebuttal?"

He smiled calmly. "I have great respect for Mr. Munger, but on this we disagree. Cryptocurrencies are not replacing national currencies, they are emerging as a new monetary hedge for younger generations against irresponsible inflationary policies. Much like equities have been during previous periods of monetary instability. They channel animal spirits away from destructive outlets."

Munger jumped in, "Animal spirits my foot! Your analogies are bunk. Cryptos have corrupted noble notions of currency and value. When inflation hits, wise heads buy land and gold, not imaginary internet coins!"

"The youth may prefer digital gold to archaic gold," the economist replied. "We cannot turn back the clock on innovation. Rather than ban them, why not create a proper regulatory framework around cryptocurrencies to build integrity, like we have done with every new financial innovation in history?"

The two continued spiritedly debating the dynamics of monetary policy, generational preferences, speculation, fraud prevention, and more. The economist emphasized the potential for cryptos to provide young people an alternative safe haven asset amidst irresponsible government debts and money printing. Munger scoffed at the idea of replacing the dollar with "computer gibberish," suggesting that reining in deficits would obviate the need for hedges, digital or otherwise.

As time wound down, the moderator asked for closing statements.

Munger concluded, "Innovation and progress arise from productivity, not speculation. Cryptocurrencies are a parasite on our economy, facilitating illegal activity while wasting brilliant minds on financial games rather than advancing civilization. If we ignore this infection, it will not end well."

In contrast, the economist offered an optimistic vision: "Cryptocurrencies, blockchain and Web3 represent both challenges and opportunities. With prudent regulation, central bank partnerships, and an openness to evolve, we can build this new frontier of finance to serve societal needs rather than undermine them. The future lies not in clinging to the past but in embracing change while bolstering ethical foundations."

As the two men shook hands briskly amidst the audience's lively applause, it was clear the debate on crypto's ideal role would continue for years to come. But with such vigorous discussion from both sides, resolutions could emerge that integrate the best of innovation within humanity's highest shared values.” To be continued…..

Less emotively, and recognising that advisors also have to bend to the considered views of the most important person in the room, the client, we have prepared a less emotional version:

The case against Bitcoin in a portfolio:

Investment advisors should think twice before suggesting any bitcoin exposure for conservative retail investors. Cryptocurrencies are still a highly speculative asset with no intrinsic value or long-term track record for risk-adjusted returns. They introduce unnecessary volatility and tail risks that most retail investors underestimate. And loses are more psychologically painful than foregone gains to mainstream clients. While bitcoin is innovative, too few understand how it works or its economic viability relative to fiat currencies. Until the industry matures further, cryptocurrencies have no place in a prudent retirement portfolio and advisors should shield clients rather than promote these experimental digital tokens.

The case for:

Prudent risk management would suggest retail investors allocate a very small portion, perhaps 1-2%, of their total portfolio towards bitcoin. While highly volatile, bitcoin has shown the ability to provide non-correlated diversification and substantial upside in bull crypto markets. For the more speculative portion of a portfolio, a modest bitcoin allocation gives retail investors controlled exposure to digital currency innovation. So long as it remains a tiny fraction of assets, the risk can be tolerable and may boost long-term returns.

Under scoring the last point we will leave you with the observed volatility of Bitcoin vs Gold and World Equities of the last five years. Note that this is a relatively advantageous starting and that most retail investors invested much nearer the top of the chart shown above, which is what attracted Charlie Munger’s ire. Either way ‘volatility’ (in terms of standard deviation) of 60% implies that one should expect Bitcoin to be up or down 60% approximately one year in three. That suggests that if you were happy to have 10% of your portfolio in Gold then a number like 1 or 2% might be equivalent. We would suggest that equities get a much higher weight as they have growing cash flows and we can offer a reasonable basis as to why they may be relatively cheap or expensive. We can even give you a pretty good idea how much you might make for investing in equities over the next 10 years. The same cannot quite be said of Gold and as far as Bitcoin is concerned we have absolutely no idea.

Nevertheless, this is something we look forward to unpicking more with Andrew Hunt in the coming weeks as we don’t think there is anyone more qualified in the world to adjudicate on this.

.webp)