What we are working on

The H&B Wealth Symposium Queensland last week marked the start of the conference season, and we were surprised to note that there is a consensus among our peers. Cyclical areas such as emerging markets and global small companies represent pockets of value, while the US, successful as it is, could be somewhat overvalued. Normally, this would be concerning as ‘crowded trades’ often portend trouble. However, in this case, it's probably just educated investors doing their calculations, thinking long-term, and arriving at a similar conclusion. It also aligns with our intuition that liquidity trends have been particularly influential recently, boosting certain very liquid, US-domiciled parts of the market more than others. Near the end of the conference, there was an interesting debate about active vs. passive investing, which we think is related to these themes. Rather than weigh in directly we kept our powder dry and have weighed in with some charts in this week’s video.

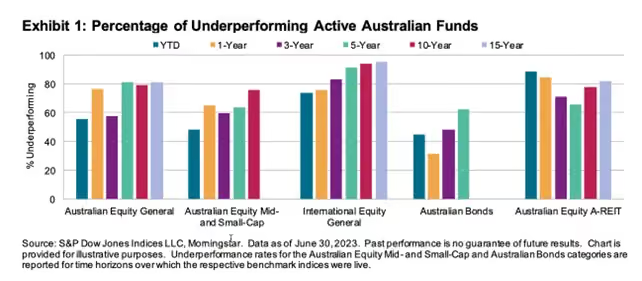

To set the scene, an adviser quoted the SPIVA statistics produced by S&P, shown in the table below.

At first glance, they seem fairly uncontroversial, yet active managers generally seem to be able to make a compelling case given the opportunity set facing them, some would say against the odds. We think that everyone may have a point. Active management has indeed struggled over the past 15 years, but there might be extenuating factors, and it is possible that the headwinds of the last 15 years could one day (perhaps soon enough) become tailwinds. We delve into this in detail in this week’s video, but the highlights are as follows:

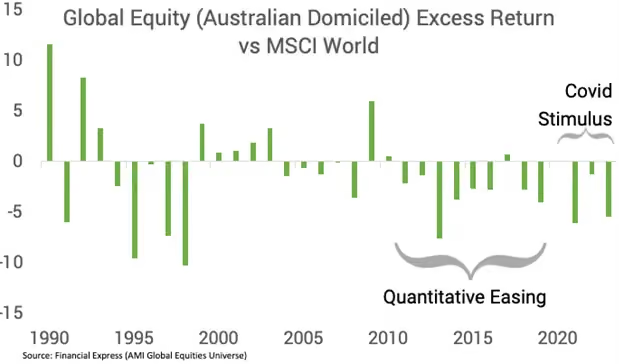

Many active managers tend to lean against market trends and bubbles near the end of a cycle due to concerns over valuations. This can lead to short-term underperformance but outperformance after the bubble pops. There is evidence this happened around the dot-com bubble and the Global Financial Crisis.

Just as the average active manager leaned against the market leaders at the end of the Dot Com Boom and then the China-sponsored commodity super cycle, the majority of broad international equity managers today are underweight mega-cap tech stocks (e.g., Facebook, Amazon) that have led markets recently, as well as the US itself (on valuation grounds). This suggests that perhaps history is repeating itself, and maybe many underperforming managers are just doing their job.

Unconventional monetary policies over the past 15 years, especially since COVID, may have distorted markets and lifted prices of certain assets like mega-cap tech stocks. This environment may have disadvantaged active managers focused on fundamentals. There are signs this liquidity-driven environment may not be able to continue forever.

If liquidity trends fade, valuations matter more, and we see some reversion to the mean from mega-cap tech, conditions could improve for fundamental active managers. However, these are just probabilities, and we don’t really know when or if the environment will change. That is why we like to use passive funds as a core and then use very active funds to manage these risks and lean into specific areas where maybe the math clearly doesn’t add up.

It might seem like we are letting active managers off the hook, and it is far from obvious that there has ever been a period when active management has dominated. However, we think it is quite possible that the scales might have been tipped by monetary policy in the last decade and a half. Overall, this is somewhat of a sideshow as forward-thinking, fundamental investors should be assessing the opportunities that lie ahead of them on their merit. But we suspect that many advisers, and perhaps their clients, will find some comfort in the admittedly dismal track record of active managers in recent years, which is not just down to greed and hubris (although that can also be a factor).