What We Are Working On

Like many in the industry we are using the January slack tide to get ahead on a few (we think) exciting software and infrastructure projects that we hope to be rolling out to clients in the next few months but there is a sense that markets will also keep us occupied from the get-go. As mentioned before Christmas it has been our intention to publish 3 ‘start of the year’ pieces reviewing 2023, previewing 2024 and reflecting on the investing regime of the next 10 years, with 1-pager client versions for each. Clients will receive these in the next few weeks via the Portal but in the meantime, here is an updated version of the 2023 Year In Review that we published just before Christmas with full year numbers. Feel free to use this as a basis for your own client collateral.

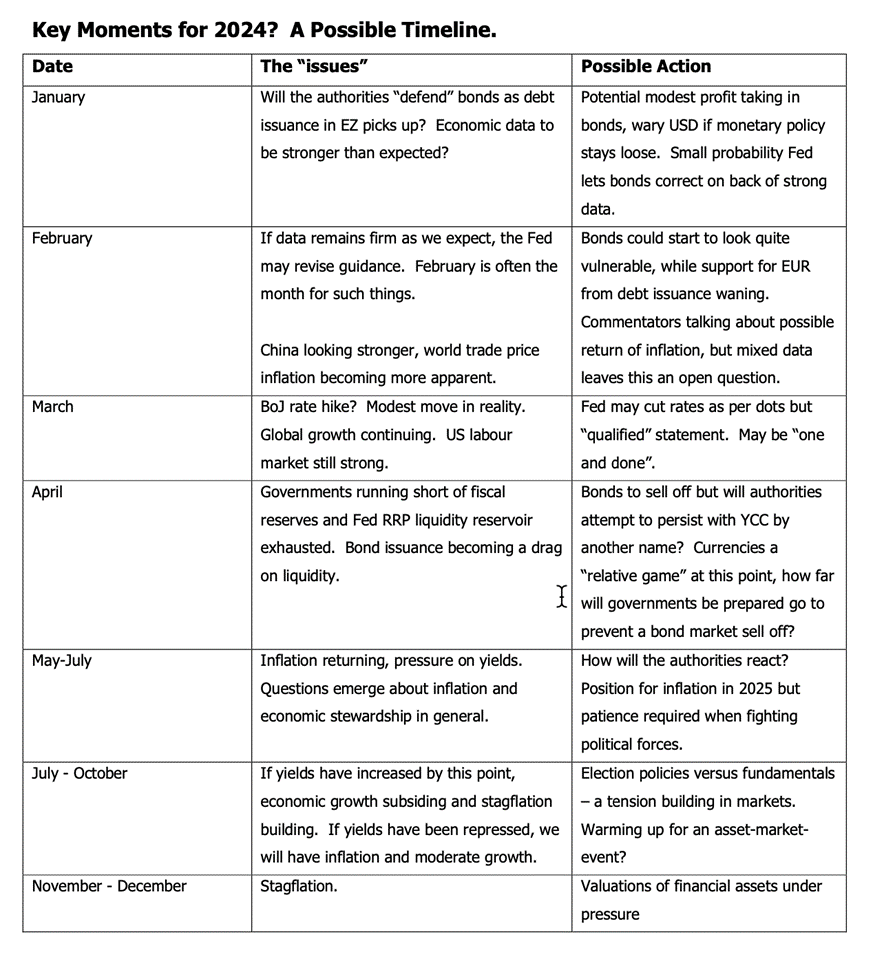

Later in the week we will be talking to Andrew Hunt about his views for 2024 and beyond, but he has already jumped the gun on us and produced an unusually detailed and even prescriptive account of what could happen in the next 12 months. Up to around nine months ago he had been unusually respectful of the inherent uncertainty in economies and markets, talking more about ‘knife edge equilibria’ and probability-based scenarios than deterministic projections. Then around April/May he broke cover and gave us the following table which started to put a more linear framework around how things might develop. One of the galling things about this time of the year is that you hear a lot from people who meticulously mapped out the market happenings of the prior year while those that, quite understandably, got it wrong are conspicuously absent. A year ago, 85% of economists (and ourselves) thought there would be a US recession in 2023. The 15% evidently have a strong voice! In the video we did with Andrew he concedes that in the end he was directionally right but perhaps for the wrong reasons. We think his 2-quarter outlook as shown in the table still resonated and provided good framework to understand markets. Like Napoleon we are just as ‘happy with lucky generals as good ones’ although both is preferable!

This week he has gone a step further and outlined a possible month by month (!) timeline for markets in 2024.

That is certainly more than we asked for and we commend him for the analytical candour but we fully expect this to change as the year progresses. We are taking particular note now as his analysis of liquidity trends last year and especially from October onwards has proved prescient. He has also become increasingly strident in recent weeks. In his words, "markets have been played by the authorities. The rally in bonds since October was entirely contrived and it has unleashed a wave of liquidity into financial markets.” This would imply that the recent rally may be built on rather different fundamentals than the mainstream financial community believes and in fact we have been almost bombarded by articles about the impact of the run down in the reverse repo facility that he brought to our attention in the last few months. As a reminder, that is the dam of liquidity where much of the excess ‘COVID response’ monetary and fiscal liquidity ended up. This amounted to over USD 2 trillion and is is now down to a mere USD 800bn and falling rapidly. We think that the change in market sentiment may well be down to a wider appreciation of this in the markets and we’re looking forward to discussing this with Andrew again. More about that next week.

Along with the 2023 Year In Review piece we will also be doing a comms piece on peer group performance, including that of industry funds but in the meantime we noticed an article in the AFR in the past few days entitled “Super balances grow almost 10pc thanks to tech rally” that managed to include both of the following 2 sentences:

“Balanced options are the most common default investment choice in superannuation funds and, by SuperRatings’ definition, means options with 60 to 76 per cent of their portfolio in growth assets.”

“Another research house, Chant West, reported that the median growth super fund, by their definition (61 to 80 per cent invested in growth options) returned 9.5 per cent for 2023. This was significantly higher than the 8.8 per cent it predicted in mid-December.”

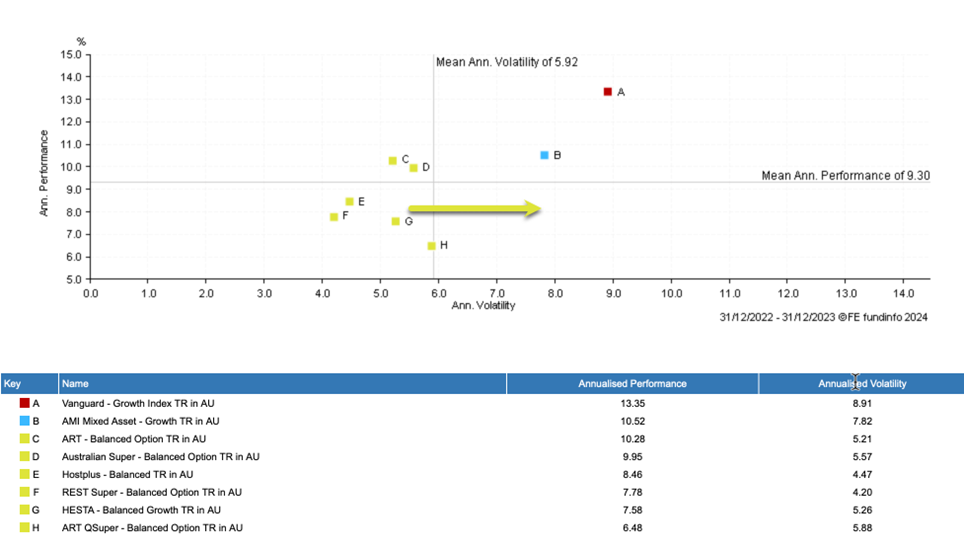

Most readers will also be aware that most options called ‘Balanced’ (and shown in the graph below) typically have allocations to growth assets of around 80%. Confused yet? We are sure clients probably are (or more worrying they may not and should be). When the industry found data is in, near the end of the month or more likely in February, we will try and decipher some of this gobbledygook and publish a piece that lines up the oranges and apples in a reasonably clear way.

In the meantime, here are a couple of graphs that show how things are shaping up.

Note first of all that this could be viewed as unrepresentative as industry funds have merely been giving up the relative gains they made in 2022. However the flip side of that is that that those returns were, with hindsight, flattered by stale pricing of illiquid assets. As these direct investments slowly reprice that has caused performance to lag in 2023.

Equally one might argue that industry funds, as a group, are exhibiting lower levels of volatility. But again, if you consider that around 30% of these portfolios is not exhibiting any volatility because its doesn't price very often (even though the risks clearly exist), and so increase observed volatility levels by 30% then you would end up with a similar level of risk. Sorry Dorothy, there is no magic. More to follow.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)